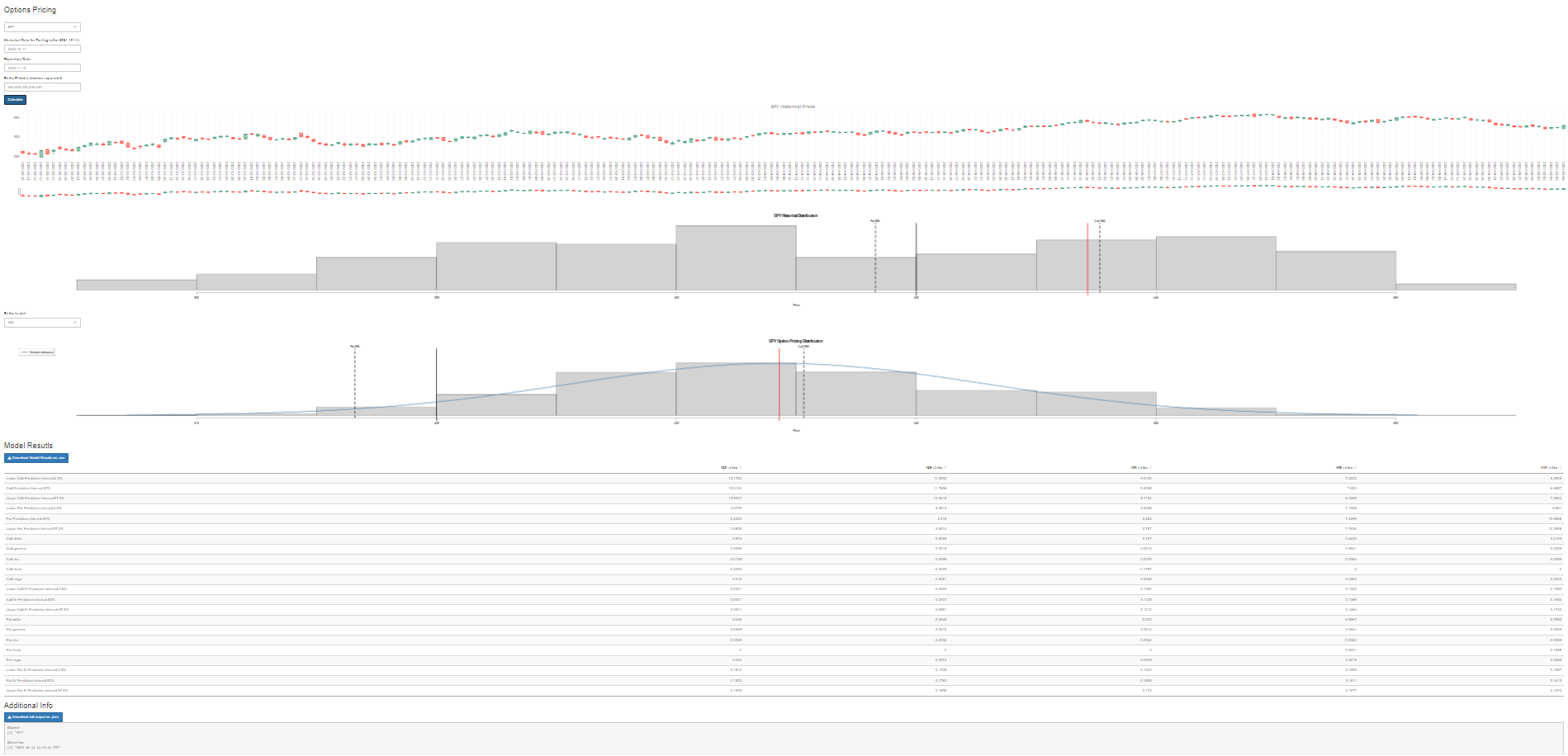

Price options without assuming the distribution — and read the tail signal hiding inside the IV.

Most options workflows — and the AI rebuilds of them — start at Black-Scholes and calibrate parameters until the model fits the quoted surface, assuming the shape of the distribution before they ever look at it. OVVO Labs starts from a different place: the empirical distribution, transformed to satisfy risk-neutrality, with call value measured through the upper partial moment above each strike and put value through the lower partial moment below it. No calibration, no normality assumption.

Each output gives you model-free implied volatility, a fair-value estimate with an empirical confidence interval, and the full Greeks — so you can see where the market is trading relative to a defensible range rather than a curve-fit surface.

The put/call IV ratio is a tail-risk state variable — not a sentiment gauge. It’s usually read as a crude directional indicator. Our research shows it does something far more useful: it tells you which tail of the return distribution turns active after a large move, and how that tail builds over the following days. Across TSLA, MSFT, MSTR, and SPY — strictly out of sample — a large up-move in a call-dominated regime is repeatedly followed by severe, fat-tailed downside that compounds for two to three weeks; a large drop in a put-dominated regime resolves into a controlled recovery. We present these as cross-asset, out-of-sample stylized facts — not curve-fit return predictions — because that is what they are.

For an advisor: when a client’s position just spiked or cratered, the IV regime tells you whether the dangerous tail is still ahead — a defensible, report-ready risk read that no sentiment indicator or Gaussian model can give you.

Annual subscription: $4,389/year. Includes annual access to the Options app and related workflow updates during the subscription period.

Want to see it on a name you care about first? Book a short walkthrough.

For institutional licensing, team access, or custom arrangements, contact us directly.