Build each client the portfolio they actually asked for.

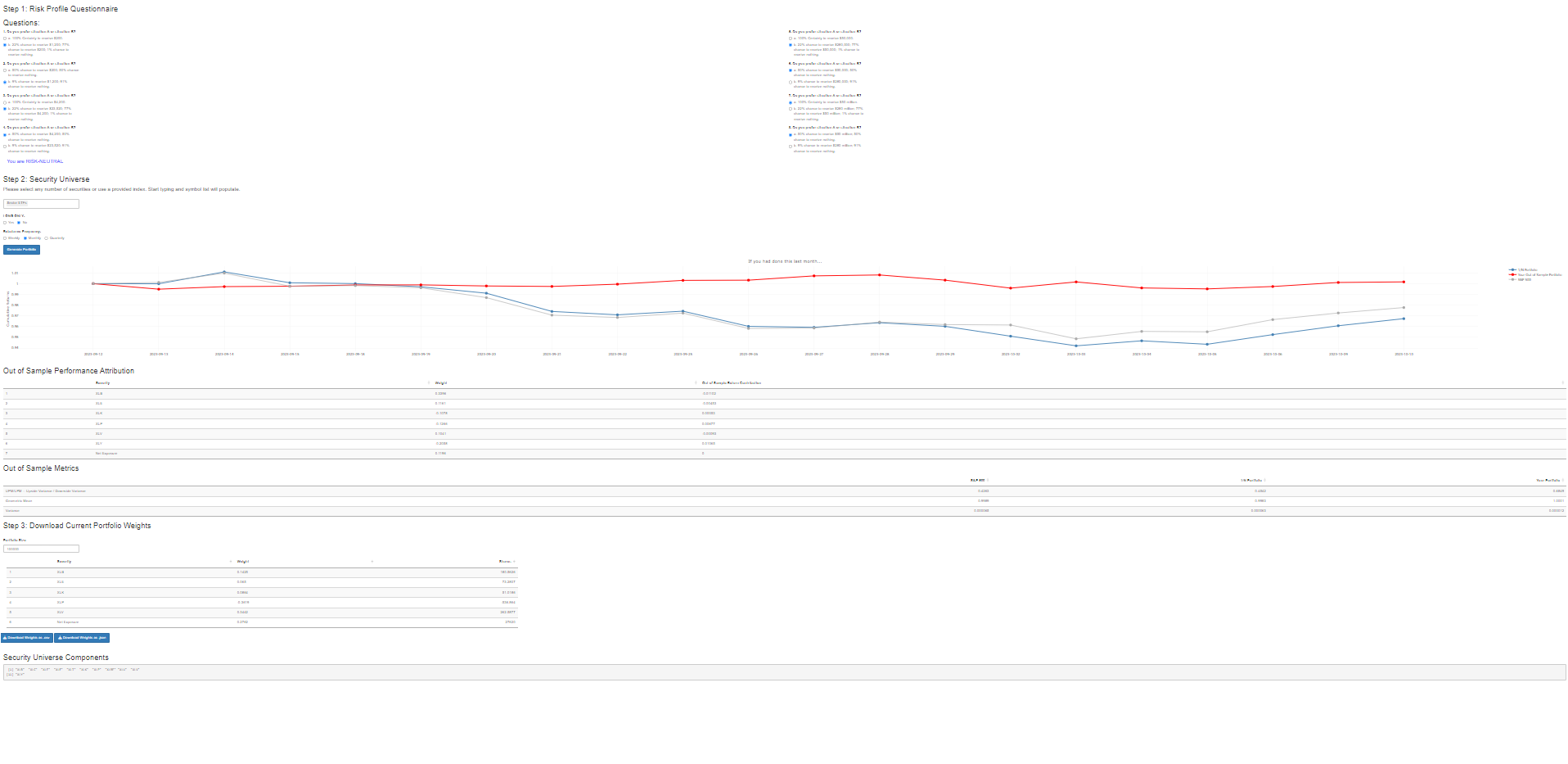

Most portfolio tools collapse a client into one of a few risk buckets and run mean-variance underneath — a model that assumes symmetric, normally distributed returns and buries downside and crash risk inside a single correlation number. When a portfolio falls harder than you told a client it would, that assumption is usually why.

Portfolio embeds each client’s real preferences — downside sensitivity, crash-aversion, upside participation — directly into a directional partial-moment covariance, before optimization, instead of bolting on a generic risk-aversion slider afterward. Upside dependence, downside dependence, divergence, and crash co-movement are handled separately, not compressed into one number.

Scale that’s real, not a toy. Optimizes a 2,000-security universe in about 20 seconds.

Tested out of sample, with no peeking. Benchmarked against naive 1/N (equal weight) and your index — usually SPY — optimized only on data through time t, and never fit through the test window. If it underperforms, you see it underperform. No curve-fitting, no cherry-picked backtest — the opposite of the overfit black boxes being sold now.

Defensible to your clients and your CCO. Peer-reviewed, validated by the Nobel laureate who created modern portfolio theory, and built on the open, inspectable NNS framework — not an AI black box you can’t explain.

Annual subscription: $5,489/year.

Want to see it on your own book first? Book a short walkthrough — we’ll show your current optimizer and OVVO Labs building the same client, side by side.

For institutional licensing, team access, or custom arrangements, contact us directly.